Energy Storage Systems Face Price Hikes: Industry Transformation Under China’s Policy Adjustments and Supply Chain Disruptions

In recent years, the prices of battery energy storage systems have continued to decline, providing strong momentum for the global energy transition. However, since the beginning of 2026, a series of policy adjustments and geopolitical events have quietly altered this trend. The price of lithium carbonate has doubled, China has abolished export tax rebates for batteries, and the US-Iran conflict has disrupted supply chains. Under the combined impact of these factors, the energy storage industry is undergoing an unprecedented price transformation.

I. Weaning Export Tax Rebates: The Underlying Signal of China’s Policy Adjustments

Starting from April 1, 2026, China will reduce the VAT export refund rate for battery products from 9% to 6%, with plans to completely abolish it by January 1, 2027. This policy covers a wide range of products, including core energy storage categories such as lithium primary batteries, lithium-ion batteries, and vanadium redox flow batteries.

As the world’s largest battery supplier, China’s policy adjustment has profound implications for the global energy storage market. The two-phase approach in the policy essentially provides a buffer period for the industry, guiding the battery sector to reduce its reliance on subsidies, curb cutthroat price competition, and shift the industry focus from price wars to technological and quality competition. In the short term, the policy directly increases corporate export costs, imposing significant survival pressure on small and medium-sized enterprises dependent on low-price strategies; in the long term, this “proactive regulation” will accelerate industry consolidation and drive competitiveness toward core strengths such as technology, brand, and supply chain integration.

II. Strong rebound in lithium carbonate prices: Accelerated transmission of upstream cost pressures

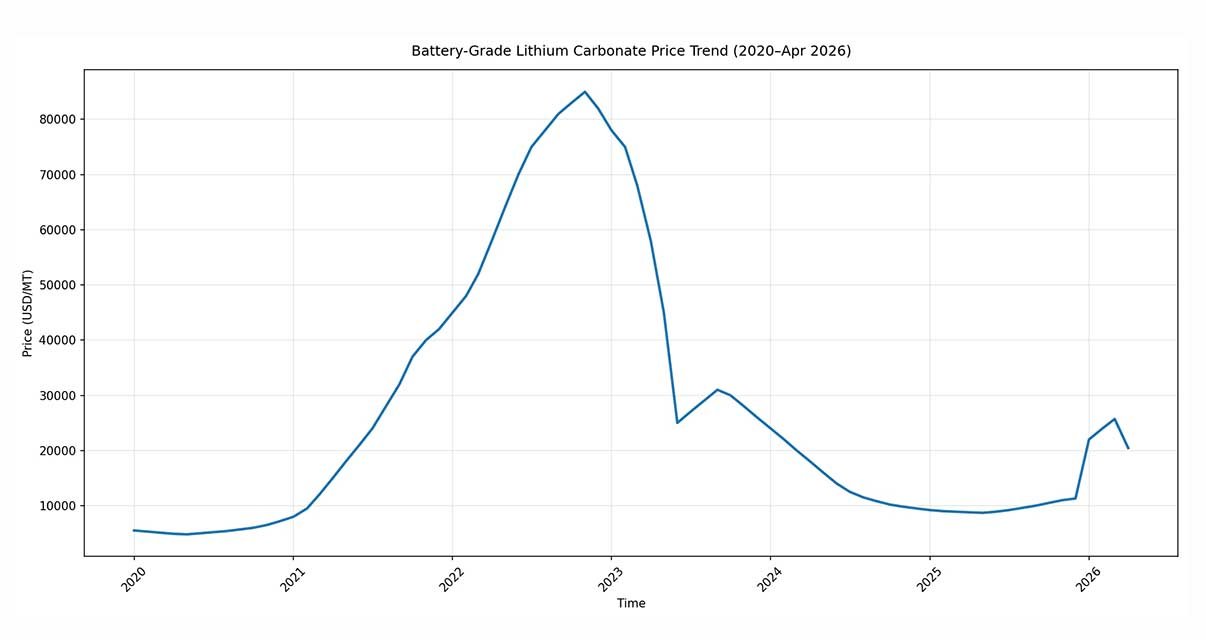

The sharp fluctuations in raw material prices serve as another key driver behind the rising costs of energy storage systems. Battery-grade lithium carbonate has rebounded strongly from its historical low of ¥75,000 per ton in late 2024, doubling to ¥150,000–160,000 per ton by the second quarter of 2026. Meanwhile, copper prices surpassed ¥90,000 per ton, lithium hexafluorophosphate prices surged by 20%, and the electrolyte solvent DMC price climbed from ¥4,000 per ton to over ¥6,000 per ton.

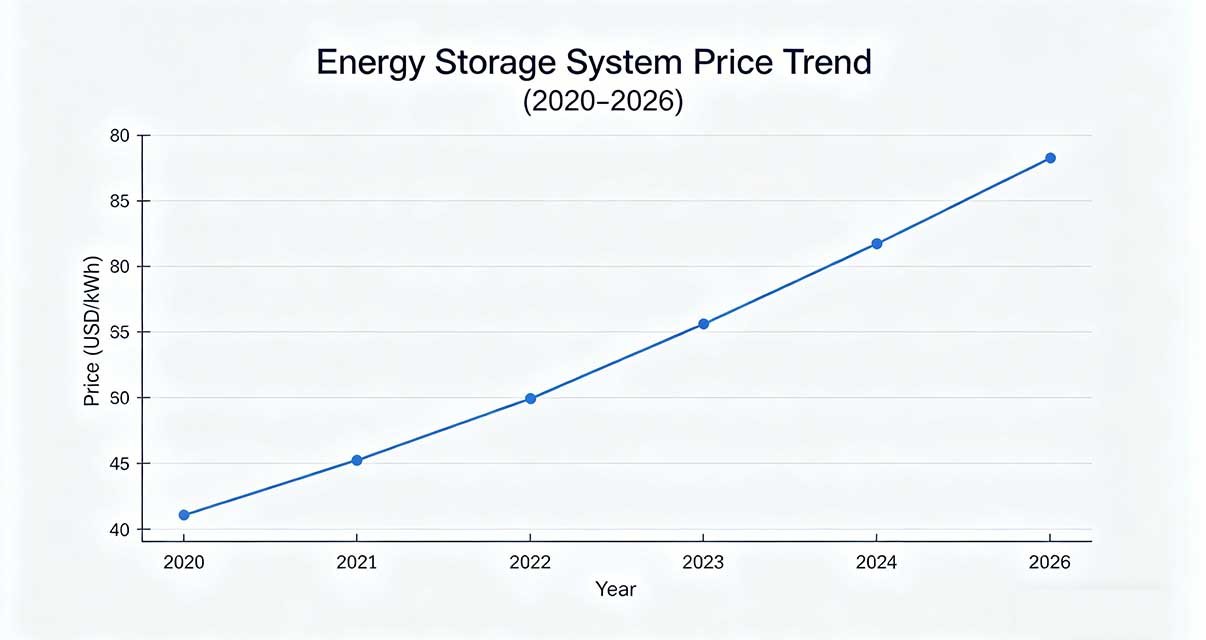

Although the current price of lithium carbonate is far below its peak of 600,000 yuan per ton in 2022, the cost impact of the price hike has already become evident. Lithium carbonate accounts for approximately 5% of the total cost of battery energy storage systems, and the comprehensive price increases in upstream supplies have directly driven up the production costs of energy storage batteries. According to InfoLink data, as of March 2026, the pricing range for China’s lithium iron phosphate energy storage cells continued to rise: the tax-inclusive price for 280Ah cells ranged from 0.340 to 0.400 yuan/Wh, while that for 314Ah cells was between 0.335 and 0.395 yuan/Wh.

III. Escalating Supply Chain Disruptions: Dual Pressure from Geopolitical Conflicts and Logistics Costs

The outbreak of the US-Iran conflict further drove up energy prices and disrupted global supply chains, exacerbating overall inflationary pressures. Laurens Vanochten, Head of Battery Storage Systems at independent power producer R.Power, noted that in addition to export tax rebates driving up prices, unpredictable factors such as transportation costs and disruptions in logistics chains also play significant roles—last year’s Suez Canal blockade being a prime example.

The uncertainty in the supply chain, coupled with robust market demand, has led to a situation where the energy storage industry faces a shortage of supplies despite ample funds. In the first quarter of 2026, China’s lithium-ion battery shipments for energy storage reached 215 GWh, a year-on-year increase of 139%. Leading manufacturers operated their production lines at full capacity, with orders generally scheduled through the end of 2026 or even the second quarter of 2027. The price of mainstream 314 Ah lithium iron phosphate cells rose from 0.26–0.31 yuan/Wh at the end of 2025 to 0.36–0.39 yuan/Wh, with some major manufacturers quoting prices exceeding 0.4 yuan/Wh—a surge of 25%–35%.

IV. The Underlying Logic Behind the Price Increase: A Fundamental Reversal in Supply and Demand Relations

The rebound in energy storage system prices is not merely a short-term fluctuation, but rather the result of a fundamental reversal in supply-demand dynamics. In the first quarter of 2026, the energy storage industry officially ended three consecutive years of price declines and entered a systemic price appreciation cycle.

From the demand side, the deepening of China’s power market reform has truly realized the value of energy storage. Regions like Inner Mongolia have secured higher and more stable returns for energy storage projects through capacity compensation mechanisms, with numerous provinces adopting similar approaches. From January to March 2026, domestic energy storage bidding volumes surged 92% year-on-year, fully igniting market demand. Meanwhile, the explosive growth in demand for AI data center (AIDC) energy storage has become a new growth engine for the industry.

From the supply-side perspective, after two years of addressing overcapacity and reducing inventory, outdated production capacities have been systematically phased out, significantly enhancing industry concentration. In the first quarter of 2026, the energy storage bidding market experienced rapid year-on-year growth, with explicit requirements for large-capacity cells of 314Ah or above, further tightening market supply and driving continuous price increases for systems.

V. moPower’s Response Strategy: Seizing Opportunities Amidst Change

In response to this wave of energy storage price increases, moPower is proactively adapting to market changes by leveraging its decades of industry expertise and specialized energy storage solutions. As a leading player with extensive experience in the energy storage sector, moPower has a deep understanding of the industry dynamics shaped by both policy incentives and market forces.

At the product level, moPower continuously refines its energy storage system solutions, reducing system costs through technological innovation to deliver more cost-effective energy storage products to customers. Strategically, the company actively expands into overseas markets, capitalizing on the historic surge in global energy storage demand. In terms of service, moPower focuses on full lifecycle value management, helping customers achieve optimal return on investment during price hike cycles.

VI. Outlook: The Return to Long-Term Value Amid the Price Hike Wave

Several industry experts believe this round of price increases is not a negative development. Although the decline in energy storage system prices in recent years has not been linear, lithium-ion batteries continue to set the benchmark for price competitiveness compared to other grid-side energy storage technologies. The price recovery will help the industry escape the quagmire of low-price competition, encouraging companies to allocate more resources to technological R&D and quality improvement.

The energy storage industry is undergoing a profound structural transformation, shifting from a “price war” to a “value war.” For moPower, this presents both challenges and opportunities. The company will continue to prioritize technological innovation and global expansion, delivering high-quality products and services to jointly usher in a new era of high-quality development for the energy storage sector.

Keywords: Energy storage system pricing, battery export tax rebate, lithium carbonate price, energy storage industry trends, moPower energy storage, energy storage system solutions