The Middle East conflict, skyrocketing electricity prices, and household energy storage doubling—who is reshaping the global energy storage demand landscape?

Key Insight: The global energy storage market is undergoing a profound paradigm shift in 2026. BloombergNEF forecasts that new global energy storage installations will reach 158 GW/459 GWh in 2026, representing a 41% year-on-year increase; HSBC Research has raised its 2026 installation forecast to 570 GWh, projecting a compound annual growth rate of 23% for global energy storage system capacity from 2025 to 2030, reaching 901 GWh by 2030. The Middle East conflict has accelerated this trend—energy storage is evolving from a mere “new energy complement” to a “energy security infrastructure,” with market demand shifting from being driven solely by policy to being shaped by a tripartite synergy of “geopolitical security, economic viability, and policy support.”

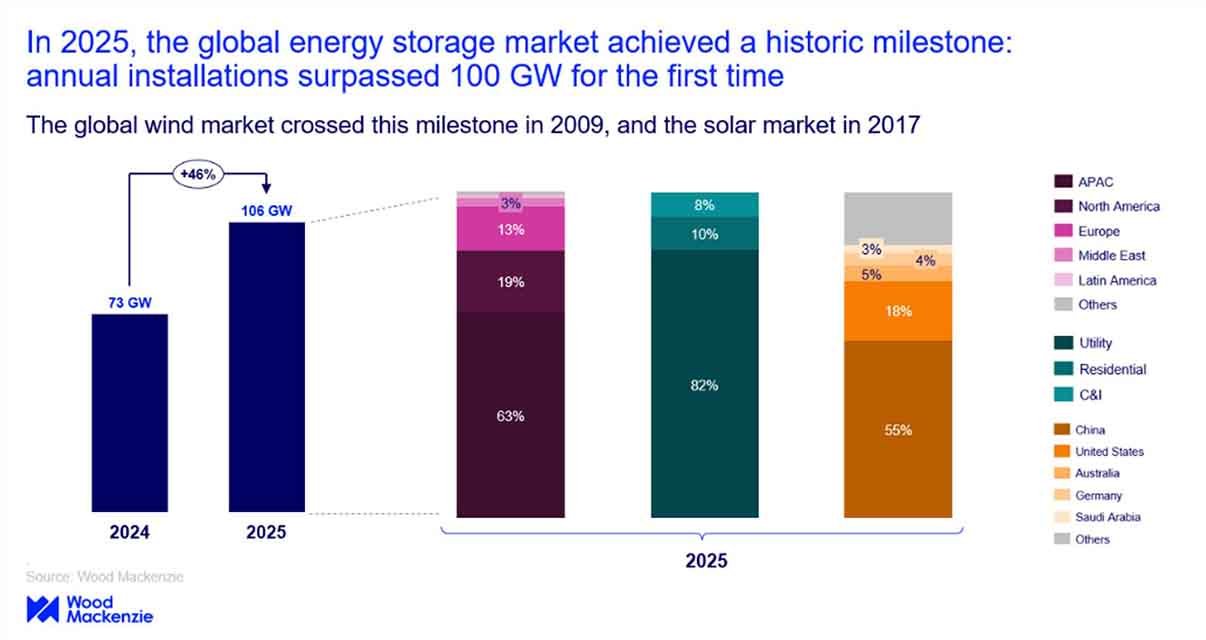

The energy storage industry achieved the leap from 10 GW to over 100 GW in just four years—photovoltaics took eight years, while wind power required fifteen years. This pace reflects not only the rapid maturation of the industry but also the new mission assigned to energy storage in the evolving global energy landscape. This article systematically analyzes the structural changes in energy storage market demand from three dimensions: global market size, regional demand characteristics, and the evolution of driving forces.

I. Global Energy Storage Capacity Expansion Accelerates: Soaring Beyond 100 GW in Four Years as Multiple Institutions Raising Forecasts

The global energy storage industry is expanding at an unprecedented pace. In 2024, global energy storage battery shipments reached 436 GWh, marking an 81% year-on-year increase; shipments further rose to 637 GWh in 2025. Entering 2026, multiple authoritative institutions have simultaneously raised their forecasts:

BNEF: Global energy storage capacity is projected to increase by 112 GW/307 GWh in 2025 and reach 158 GW/459 GWh in 2026, representing a year-on-year growth of 41%.

HSBC Research: The installed capacity forecast for 2026 has been revised upward to 570 GWh, with global ESS capacity projected to reach 901 GWh by 2030, achieving a CAGR of 23% from 2025 to 2020.

InfoLink Consulting: It predicts that global energy storage cell shipments will reach 801 GWh in 2026, system integration shipments will reach 600 GWh, with approximately 353 GWh of new installed capacity.

Dongwu Securities: Global energy storage installed capacity is projected to grow by over 60% in 2026, with a compound annual growth rate (CAGR) of 30%-50% from 2027 to 2029.

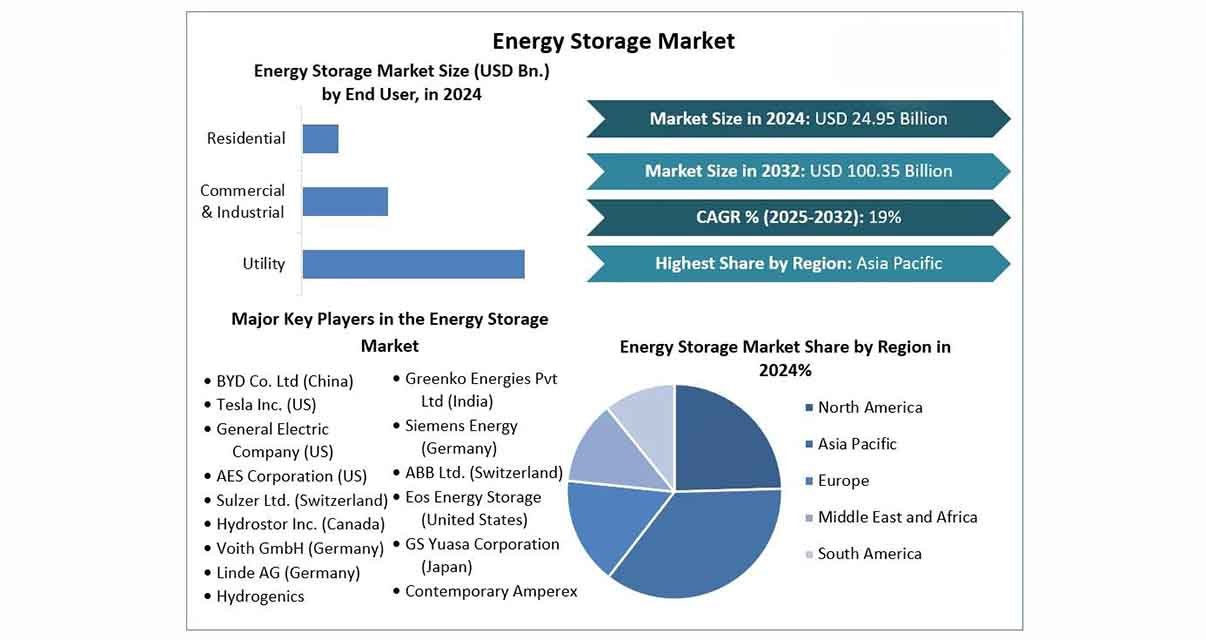

In terms of market value, the renewable energy storage market is projected to grow from $167.89 billion in 2025 to $218.53 billion in 2026, with a CAGR of 30.2%.

II. Characteristics of Regional Demand Differentiation: Formation of a Quadrupolar Driving Pattern

The global energy storage market has established a new paradigm driven by the synergistic collaboration of “China, Europe, the United States, and emerging markets,” with distinct regional demand characteristics exhibiting significant differentiation.

Europe: The Surge in Household Energy Storage Driven by Economic Factors. Since the beginning of 2026, demand for household energy storage in Europe has remained robust, with installation volumes accelerating rapidly in key markets such as the UK, Germany, and the Netherlands. Escalating geopolitical conflicts have driven up natural gas and electricity prices; Dutch TTF natural gas futures have risen by over 100%, significantly shortening the payback period for household energy storage investments. fueled by the restructuring of the energy landscape and the refinement of policy frameworks, global household energy storage is transitioning from being primarily subsidy-driven to being driven by economic viability and market forces. 2026 is expected to be a pivotal year for the large-scale deployment and commercialization of household energy storage. Frost & Sullivan forecasts that the global household energy storage market will exceed RMB 80 billion in 2026, representing a year-on-year growth rate of over 125%.

The Middle East: Conflict is accelerating rather than reversing the transition to new energy. According to an S&P Global report, the clean energy strategies of Gulf countries—particularly Saudi Arabia and the United Arab Emirates—have not undergone significant adjustments due to the war. Saudi Arabia aims for renewable energy to account for approximately 50% of its energy mix by 2030, while the UAE plans to triple its clean energy installed capacity during the same period. Saudi Arabia has tendered nearly 30 GWh of battery energy storage projects, with about 8 GWh already operational by the end of 2025. However, the situation in the Strait of Hormuz has begun to affect equipment delivery timelines for some projects, though the time-sensitive clauses in the Power Purchase Agreement (PPA) contracts make delays manageable. SMM estimates that the annual demand for energy storage cells in the Middle East will reach approximately 50 GWh in 2026, accounting for 6% of global demand.

China: The world’s largest incremental market, leading in both technology and market share. In 2025, China’s newly installed capacity for advanced energy storage reached 65 GW, representing a year-on-year increase of 52%. Chinese companies dominate the global energy storage supply chain—of the 66 manufacturers listed in the BNEF Tier 1 Energy Storage Manufacturers list for Q2 2026,56 were Chinese enterprises, accounting for nearly 85%, covering the entire industry chain from cell manufacturing to system integration.

Emerging Markets: A Rapidly Rising New Growth Pole. In emerging regions such as Southeast Asia and Latin America, where weak power grid infrastructure, frequent power outages, and high electricity costs prevail, the dual demands of ensuring reliable power supply and reducing electricity expenses are driving a rapid surge in energy storage demand.

III. The Structural Transformation of Demand-Driven Logic: A Three-Tier Analytical Framework

The structural changes in the current energy storage market demand can be understood through a three-tier framework:

The First Layer: The Macro Level – Elevating Energy Security to a New Dimension

The Middle East conflict has brought energy security to the forefront of national strategy. According to World Bank projections, Brent crude oil prices will surge to $118 per barrel by 2026, with natural gas prices expected to rise by 25%. The connection between power system resilience and national security has never been stronger—energy storage is no longer merely a “regulating valve” for the grid, but rather a “strategic infrastructure” for energy security.

Second Layer: The Demand Layer – Policy and Economic Resonance Stimulate Growth

HSBC Research notes that the BNEF Tier 1 certification has become a “passport for overseas expansion” for energy storage companies, while countries are accelerating the introduction of supportive policies for the sector.

- The EU’s AccelerateEU initiative sets a target of achieving 200 GW of energy storage capacity by 2030.

- The European Commission has approved national energy storage subsidy packages worth €2 billion for Poland and €699 million for Spain.

- The UK and Australia have introduced subsidy policies to stimulate household savings demand.

Meanwhile, fundamental factors such as the widening electricity-carbon price spread and the shortened payback period for household energy storage investments are driving economic incentives to gradually surpass policy-driven motivations.

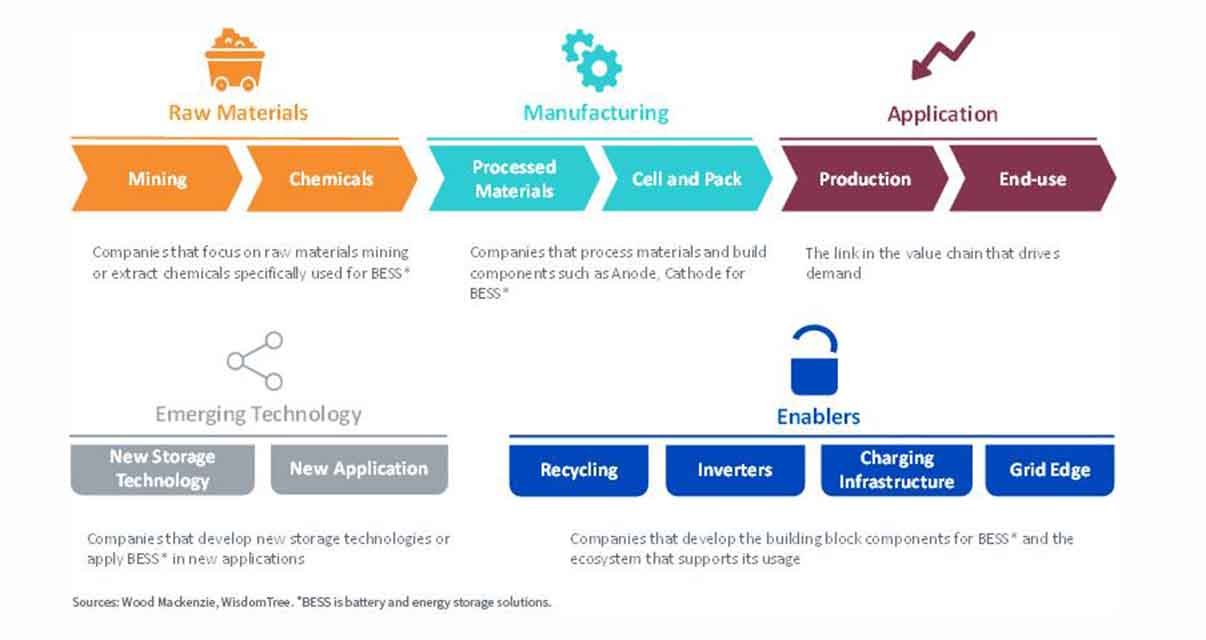

Third Layer: Industrial Layer – China Leads the Global Supply Chain

China enterprises hold a core position in the global energy storage industry thanks to their cost advantages and production capacity reserves. However, the supply chain is not without concerns—fluctuations in raw material metal prices directly impact manufacturing costs, and transportation disruptions must also be addressed in contingency plans. In the medium to long term, increased trade barriers may drive China’s energy storage industry to evolve from “product exports” toward “overseas localized manufacturing coupled with coordinated local supply chains.”

![Three-layer structure diagram of energy storage-driven logic] (Recommended accompanying image: A schematic diagram illustrating the three-tier progressive structure, demonstrating the transmission logic of “macro-level security → demand activation → industrial supply”)

IV. Summary and Outlook

The fundamental changes in the energy storage market demand can be summarized as three “upgrades”:

Role Upgrade: From “Renewable Energy Support” to “Energy Security Strategic Infrastructure”

Driven Upgrade: From “Single Policy Drive” to the Synergy of Security, Cost-effectiveness, and Policy

Level Upgrade: From “Demonstration in a Few Regions” to “Collaborative Development of Four Global Market Polars”

Looking ahead, the energy storage industry is entering an unprecedented period of rapid development. For industry professionals, understanding the structural shifts in market demand, accurately identifying regional differentiation characteristics, and continuously enhancing supply chain resilience and technological innovation capabilities will be key to capitalizing on this golden growth cycle.

MOPOWER ENERGY specializes in the global energy storage market, dedicated to delivering comprehensive intelligent energy storage solutions for households, businesses, and grid operators across all scenarios. Visit www.mopower360.com to seize the opportunities arising from evolving energy storage demands.