Ecological Construction and Development History of Lithium-Ion Batteries

Against the backdrop of the global carbon neutrality drive, the lithium-ion battery industry is embracing unprecedented development opportunities and has become a core pillar for energy transition and the new industrial system. Among them, power batteries and energy storage batteries, as the two core application sectors, account for nearly 93% of the lithium-ion battery market and dominate the development direction of the industry. From the popularization of new energy vehicles to the large-scale deployment of new energy storage, from diversified competition among technical routes to the reshaping of the global market landscape, the lithium-ion battery industry is undergoing a critical transformation from scale expansion to high-quality development.

A lithium-ion battery is a rechargeable electrochemical system that stores and releases energy through the back-and-forth migration of lithium ions between the positive and negative electrodes. With comprehensive advantages including high energy density, long cycle life and stable power output, it has become the most widely applied core solution in the energy system. Its industrial chain covers upstream mineral resources, midstream materials and battery manufacturing, and downstream application terminals, forming a complete ecological system.

The upstream is based on mineral resources such as lithium, cobalt and nickel, extending to key materials including cathodes, anodes, electrolytes and separators. The midstream focuses on cell manufacturing, battery module assembly and battery pack system integration, serving as the core link for technological innovation. The downstream covers diversified application scenarios such as new energy vehicles, energy storage systems and consumer electronics, among which power batteries and energy storage batteries constitute the dual engines of industrial growth.

In 2024, China’s output of power batteries, energy storage batteries and consumer batteries reached 826 GWh, 260 GWh and 84 GWh respectively, accounting for 70.60%, 22.22% and 7.18% respectively, clearly presenting a “two-main, one-supplementary” market structure.

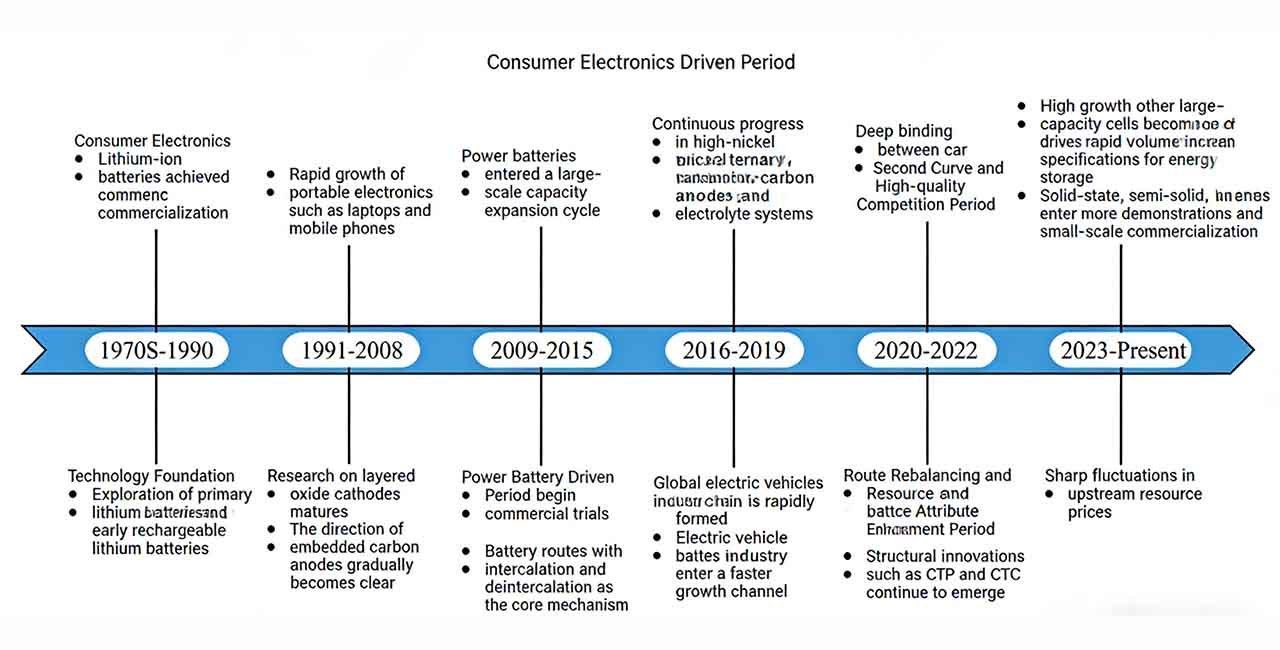

Reviewing its development history, the lithium-ion battery industry has evolved over more than half a century.From the 1970s to 1990 was the technology foundation stage: the direction of intercalation carbon anodes gradually became clear, research on layered oxide cathodes matured, and the battery route centered on lithium intercalation and deintercalation was established.From 1991 to 2008 was the consumer electronics-driven stage: lithium-ion batteries were commercialized, and the rapid growth of portable electronic devices such as laptops and mobile phones promoted the initial large-scale development of the industry.From 2009 to 2015 came the power battery-driven stage: global electric vehicles began commercial trials, and China’s power battery industrial chain took shape rapidly.From 2016 to 2019 was the large-scale cost reduction stage: automakers and battery enterprises formed deep partnerships, technologies such as high-nickel ternary materials and silicon-carbon anodes continued to advance, and power batteries entered a cycle of large-scale capacity expansion.From 2020 to 2022 featured route rebalancing and strengthened resource attributes: structural innovations such as CTP and CTC emerged, and the lithium iron phosphate (LFP) route re-emerged in passenger vehicles.Since 2023, the industry has entered the second growth curve of energy storage and high-quality competition stage: solid-state, semi-solid-state and sodium-ion batteries have entered more demonstration and small-scale commercialization phases, and the surge in energy storage installations has driven the rapid expansion of energy storage cells.

At the global market level, the lithium-ion battery industry maintains rapid growth.Global shipments of lithium-ion batteries increased from 323.2 GWh in 2020 to 1549.6 GWh in 2024, representing a compound annual growth rate (CAGR) of 48.0%.Global shipments are expected to exceed 5200 GWh by 2030, with a CAGR of 22.5% from 2024 onwards.

As the world’s largest market, China’s shipments rose from 142.5 GWh in 2020 to 1173.0 GWh in 2024, with a CAGR of 69.4%, and are projected to surpass 3900 GWh by 2030, continuing to lead the global market.In terms of regional structural changes, Europe’s share of global lithium-ion battery shipments is expected to rise from 9.8% in 2024 to 12.5% by 2030. The global lithium battery supply system is evolving from centralization to regional coordination.